Depreciation Calculation Methods

Various depreciation calculation methods are mentioned below:

i. Base Method

ii. Declining Balance Method

iii. Maximum Amount Method

iv. Multi Level Method

v. Period Control Method

i. Base Method

Base Method- SPRO> IMG> Financial Accounting (New)> Asset Accounting>Depreciation> Valuation Methods> Depreciation Key> Calculation Methods>Define Base Methods

Base method primarily specifies:

-

-

-

- The Type of depreciation (Ordinary/ Special Depreciation)

- Depreciation Method used (Straight Line/ Written Down value Method)

- Treatment of the depreciation at the end of Planned useful life of asset or when the Net Book value of asset is zero (Explained in detail later in other related transactions ).

-

-

Straight Line Method (SLM)

-

-

-

- This is the simple method of depreciation.

- It charges equal amount of depreciation each year over useful life of asset.

- It first add up all the costs incurred to bring the asset in use and then it divides that by the useful life of asset in years to calculate the depreciation expense.

- E.g.: Say a Computer costs Rs. 30,000 and Rs. 11,000 (as additional set-up/installation/maintenance expenses) = Rs 41,000 and it is anticipated that its scrap value will be Rs. 1,000 at the end of its useful life, of say, 5 yrs.

-

-

Total Cost = Cost of Computer + Installation Exp. + Other Direct Costs

Depreciable Amount over No. of years = Total Cost – Salvage Value (At end of useful life)

30,000 +11,000 =41,000 (Total cost)

41,000 – 1,000 = 40,000 as the Depreciable Amount

Depreciable Amount = Rs. 40,000, Spread out over 5 years = Rs. 40,000/5(Yrs) = Rs. 8000/- depreciation per annum.

Written Down Value Method (WDV)

-

-

-

- This method involves applying the depreciation rate on the Net Book Value (NBV) of asset. In this method, depreciation of the asset is done at a constant rate.

- In this method depreciation charges reduces each successive period.

- This method should be used in those assets, where high depreciation should be charged in initial years.

- Assume the price of a depreciable asset i.e. computer is Rs. 40,000 and its salvage value after 10 years is 0.

- In this method NBV will never be zero.

-

-

Depreciation Per year = (1/N) Previous year’s value, Where N= No. of years

So in our example, the depreciation amount during the first year is

[Rs. 40,000*1/10] =Rs. 4,000

NBV of computer after 1st year= Rs 40,000- 4,000 = Rs. 36,000

Depreciation for 2nd year is

[Rs. 36,000*1/10] =Rs. 3,600

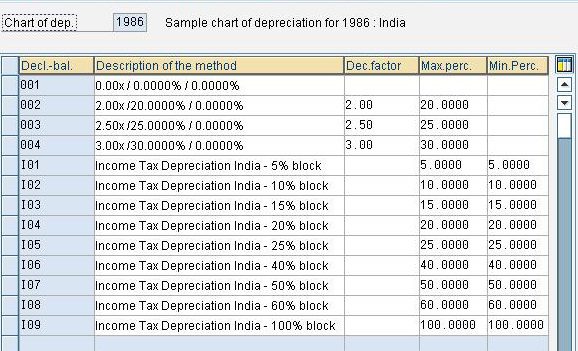

ii. Declining Balance Method

Enter Transaction code AFAMD- Change View “Declining Balance Method”

AFAMD- Change View “Declining Balance Method”- SPRO> IMG> Financial Accounting (New)> Asset Accounting>Depreciation> Valuation Methods> Depreciation Key> Calculation Methods> Define Declining-Balance Methods

This is the other name of Written Down Value (WDV) method as mentioned in Base method above.

If the WDV method is specified in Base method then the following additional settings in this method can be used:

-

-

-

- A multiplication factor for determining the depreciation percentage rate. The system multiplies the depreciation percentage rate resulting from the total useful life by this factor.

- A lower limit for the rate of depreciation. If a lower depreciation percentage rate is produced from the useful life, multiplication factor or number of units to be depreciated, then the system uses the minimum percentage rate specified here.

- An upper limit for the rate of depreciation.If a higher depreciation percentage rate is produced from the useful life, multiplication factor or number of units to be depreciated, then the system uses the maximum percentage rate specified here.

-

-

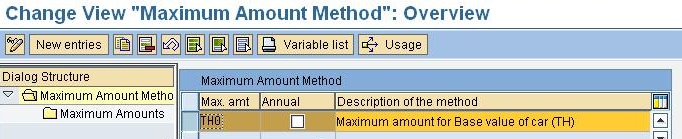

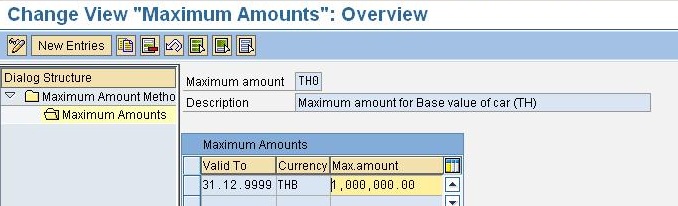

iii. Maximum Amount Method

Maximum Amount Method- SPRO> IMG> Financial Accounting (New)> Asset Accounting>Depreciation> Valuation Methods> Depreciation Key> Calculation Methods> Define Maximum Amount Method

Generally, If we uses Straight line method, then depreciation amount should be same for all years. But depreciation on asset is subject to change due to many factors e.g. any addition to the asset, change in estimate of useful life, change in estimate of scrap value etc.

So for maintaining better control on the amount of depreciation, SAP has provided this method where we can specify the maximum amount that can be charged as expense in a particular year. If this is specified, user will not be able to post depreciation exceeding the amount specified here.

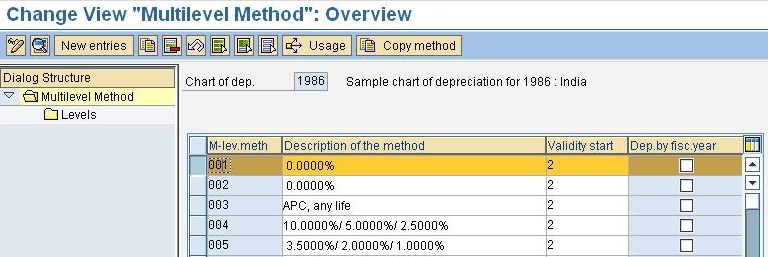

iv. Multi Level Method

Enter Transaction code AFAMS- Change View “Multilevel Method”

AFAMS- Change View “Multi Level Method”- SPRO> IMG> Financial Accounting (New)> Asset Accounting>Depreciation> Valuation Methods> Depreciation Key> Calculation Methods> Define Multi Level Methods

As the name itself suggests, this method provides the flexibility to specify different rate of depreciation for different years/periods. E.g. in some cases depreciation rate required is different in initial years and after that the rate should be changed. This can be achieved in SAP by using Multi level Method.

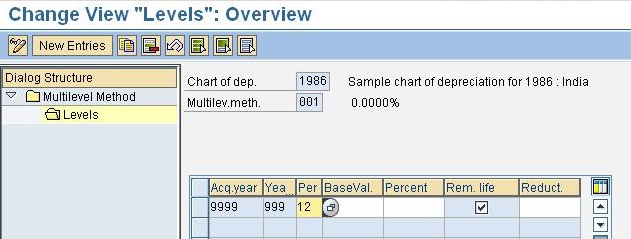

In this method, SAP provides us the possibility to specify different levels during the useful life of an asset. Each level represents the period of validity of a certain percentage rate of depreciation. This percentage rate is then replaced by the next percentage rate when its period of validity has expired. We can specify the validity period for the individual levels of a asset in years and months.

It also provides the flexibility to us to choose the defined validity period, which can begins with

-

-

-

- The capitalization date.

- The start date for ordinary or tax depreciation.

- The original acquisition date of the asset under construction.

- The changeover year.

-

-

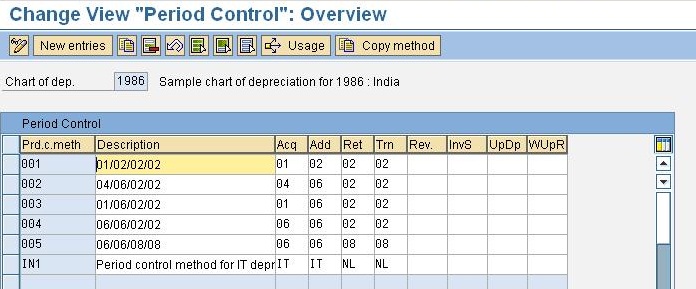

v. Period Control method

Enter Transaction code AFAMP- Maintain Period Control Method

AFAMP- Maintain Period Control Methods”- SPRO> IMG> Financial Accounting (New)> Asset Accounting>Depreciation> Valuation Methods> Depreciation Key> Calculation Methods> Maintain Period Control Methods

It is one of the most relevant method to keep control on the calculation of depreciation. Here we mention the different rules for periods in case of different scenarios for assets. This method controls the period for which the depreciation is calculated on an asset during the year.

Under this method, we can specify the period for which the depreciation should be calculated in case of :

-

-

-

- Acquisition of Asset/Subsequent acquisition

- Retirements/Scrap

- Sales/Transfers

- Upward/Downward Revaluation

-

-

There are some standard methods that has been provided by SAP e.g. Pro rata at

mid period, Pro rata at period start date, at the start of year or At mid year etc. E.g., If client requires to depreciate an asset from the First day of the year in which the asset is capitalised, we can use the method `At the start of the Year` in case of Acquisition.

This method has been explained with the help of one comprehensive example below:

Example: A company wants to charge depreciation as follows. Client follows calendar year from January-December 2013 as

Accounting/Fiscal year.

1. In case of Asset Acquisition: Depreciation should start from the First day of the year in which asset is acquired.

2. In case of Asset Addition: Depreciation should start from the Ist day of period of date of addition.

3. In case of Asset retirement: Depreciation should be charged upto Mid period regardless of date of retirement.

4. In case of Asset Transfer: Depreciation for the full year should be charged by the transferee company.

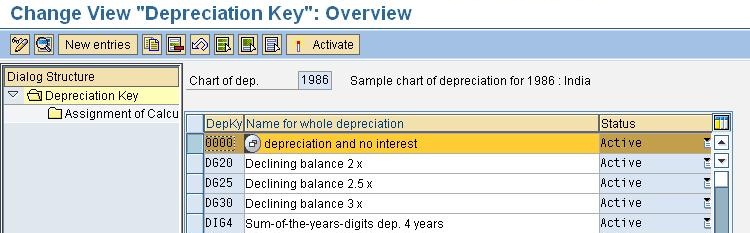

After having knowledge of all the depreciation calculation methods, we can assign the depreciation calculation methods to the depreciation key.

Creation of Depreciation key:

- Asset accounting module of SAP calculates the depreciation on Assets based on the configuration done for Depreciation key. Depreciation Key basically contains the calculation methods which in combination control the following:

- Period for which Depreciation is charged

- Method of Depreciation

- Scrap value, if any

- Planned change in Method of Depreciation

We enter a separate depreciation key for each depreciation area in the asset master record.

Creating Depreciation Key:

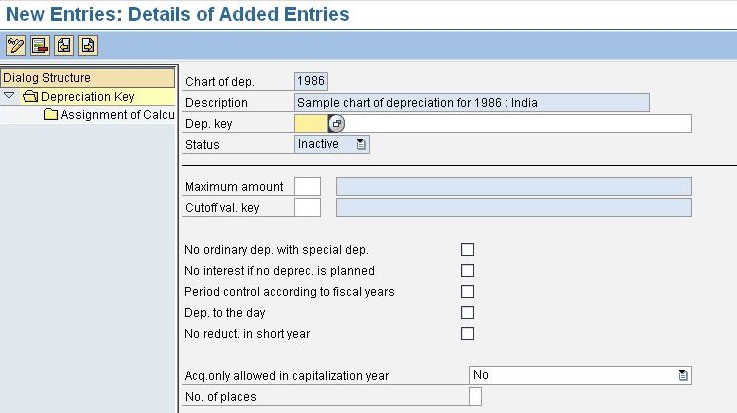

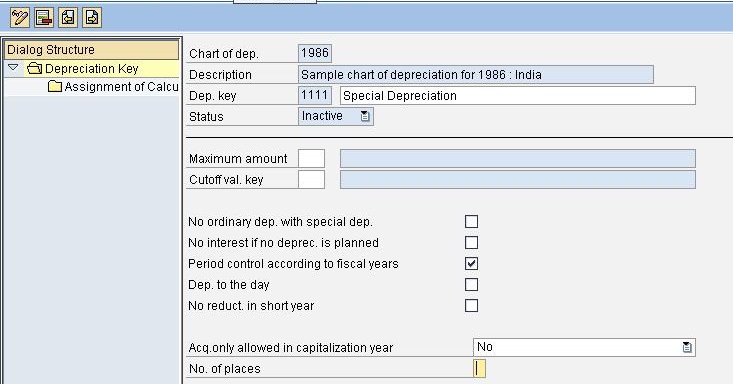

Enter Transaction code AFAMA- Change View “Depreciation Key”

AFAMA- Change View “Depreciation Key”- SPRO> IMG> Financial Accounting (New)> AssetAccounting>Special Valuation> Net Worth Tax>Depreciation Key>Define Depreciation keys

As depreciation key is Chart of Depreciation dependent, system will prompt to enter chart of Depreciation on accessing transaction AFAMA and screen shown below will be displayed.

Here, we need to specify the following at appropriate fields\check boxes:

-

-

- No./Name of Depreciation key Numeric/Alphanumeric.

- Maximum Amount method (Discussed above in methods of depreciation)

- Cutoff value key to control the scrap value if no absolute scrap value is maintained in the system. The cutoff percentage rate that is determined on the basis of this cutoff value key is only used by the system when:

- There is no absolute scrap value entered in the the depreciation areas of the asset concerned (an absolute scrap value takes precedence over a cutoff percentage rate)

- Negative book value is not allowed for the asset

-

-

-

- Whether ordinary depreciation should continue to be charged in a year in which special depriciation is also charged on the asset or not?

- Set `Depreciation to the day` indicator to allow system to calculate the depreciation according to the number of days the asset is used.

-

If this indicator is set, period control method assigned to depreciation key will be ignored and Asset value date will be considered as the depreciation start date.

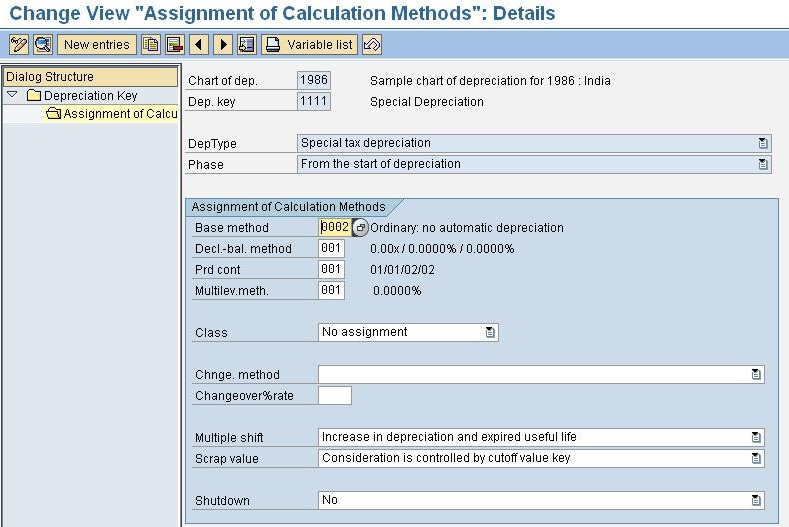

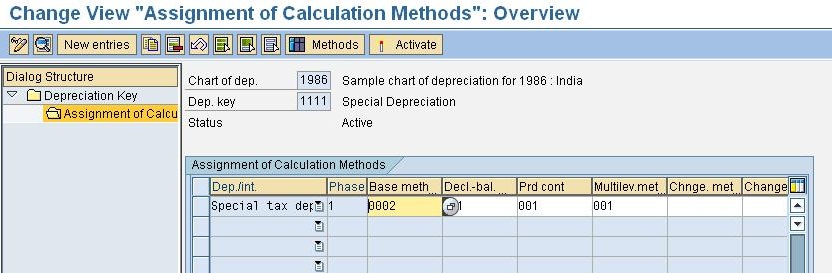

Assignment of Depreciation Calculation Method to Depreciation key:

Select The depreciation key and click on Assignment of Calculation methods. Now assign different methods to depreciation key.

Leave A Comment?

You must be logged in to post a comment.